Understanding Credit Reports in Australia: Essential Information for 2024

A credit report plays a pivotal role in an individual’s financial life, especially when applying for loans, credit cards, or even renting a house.

In Australia, understanding your credit report and its implications can significantly impact your ability to access credit and other financial products.

This article will delve into what a credit report is, how it works in Australia, what information it contains, and how you can manage and improve your credit score.

What is a Credit Report?

A credit report is a detailed record of your credit history. It includes information on how you’ve managed various credit accounts, including credit cards, loans, mortgages, and even utility bills.

This report is compiled by credit reporting agencies, commonly referred to as credit bureaus, and it serves as a tool for lenders to assess your creditworthiness.

In Australia, the three main credit reporting agencies are:

- Equifax

- Experian

- illion

These agencies collect and maintain data on your credit activities. They then generate a credit report and provide it to lenders, who use it to evaluate the risk of lending money to you.

What Information is Included in a Credit Report?

Credit reports in Australia contain a variety of personal and financial details. Here’s a breakdown of the key information included:

- Personal Information: This section includes your full name, address, date of birth, employment history, and driver’s license number. It’s used to identify you correctly and match your credit records accurately.

- Credit Accounts: Your report lists all the credit accounts you’ve opened, including credit cards, loans, and mortgages. It provides details such as the date the account was opened, the credit limit, and the status of the account (open or closed).

- Repayment History: This is one of the most crucial sections for lenders. It shows whether you’ve made repayments on time over the past two years. Missed or late payments can significantly lower your credit score.

- Defaults and Collection Notices: If you’ve defaulted on a loan or credit card, or if any debts have been sent to a collection agency, this will be recorded on your credit report. Defaults typically remain on your report for five years.

- Credit Inquiries: Whenever you apply for credit, the lender will conduct a “hard inquiry” into your credit report. These inquiries are recorded and can remain on your report for up to five years. Multiple credit inquiries in a short time can lower your credit score as it may indicate financial distress.

- Bankruptcies and Court Judgments: Any legal actions taken against you for unpaid debts, such as bankruptcies or court judgments, will appear on your report. These can significantly impact your ability to obtain credit.

→ SEE ALSO: What Is a Good Credit Score?

How Does a Credit Score Work in Australia?

A credit score is a numerical value calculated based on the information in your credit report.

It represents your creditworthiness and is a quick way for lenders to assess the risk of lending you money.

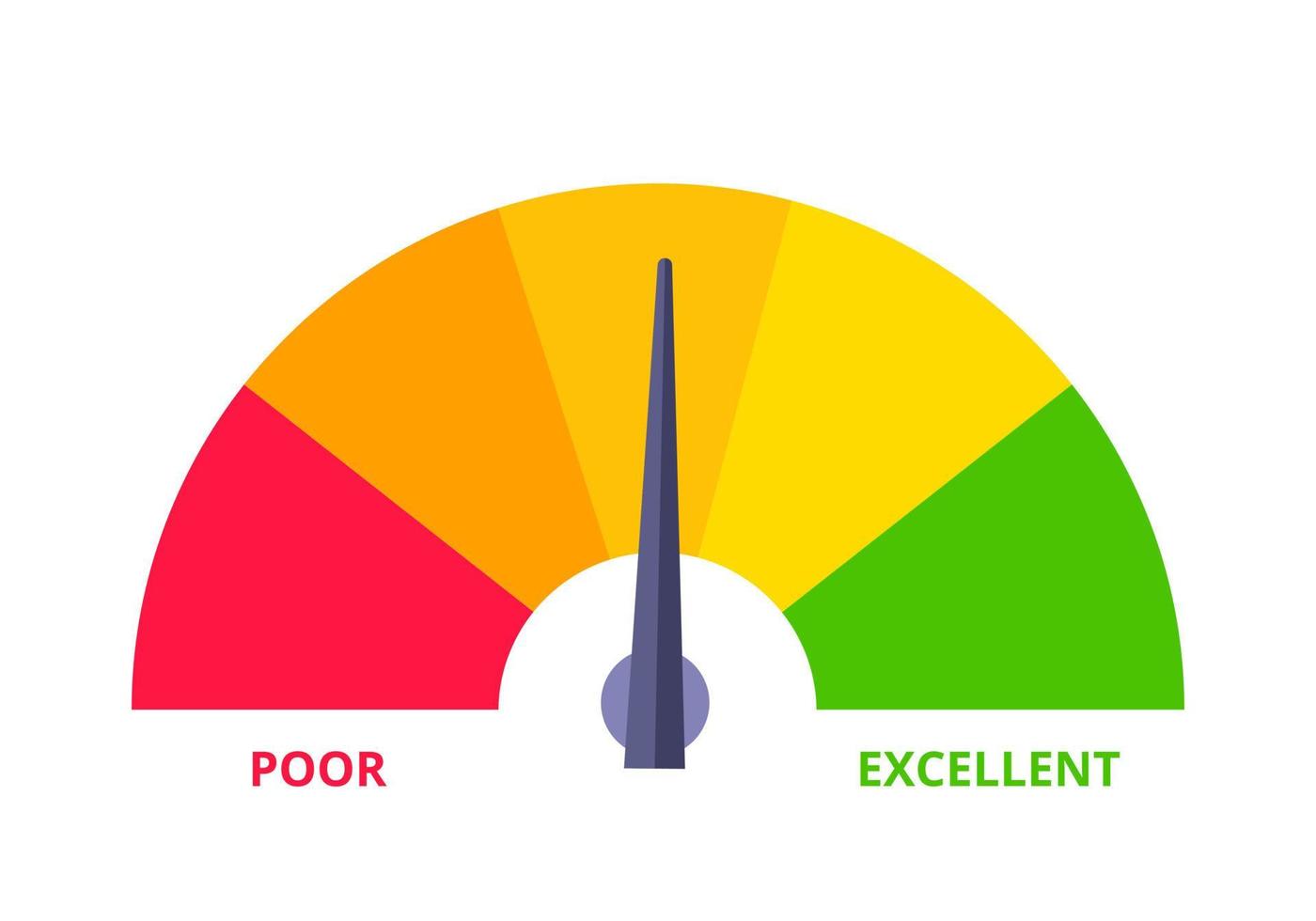

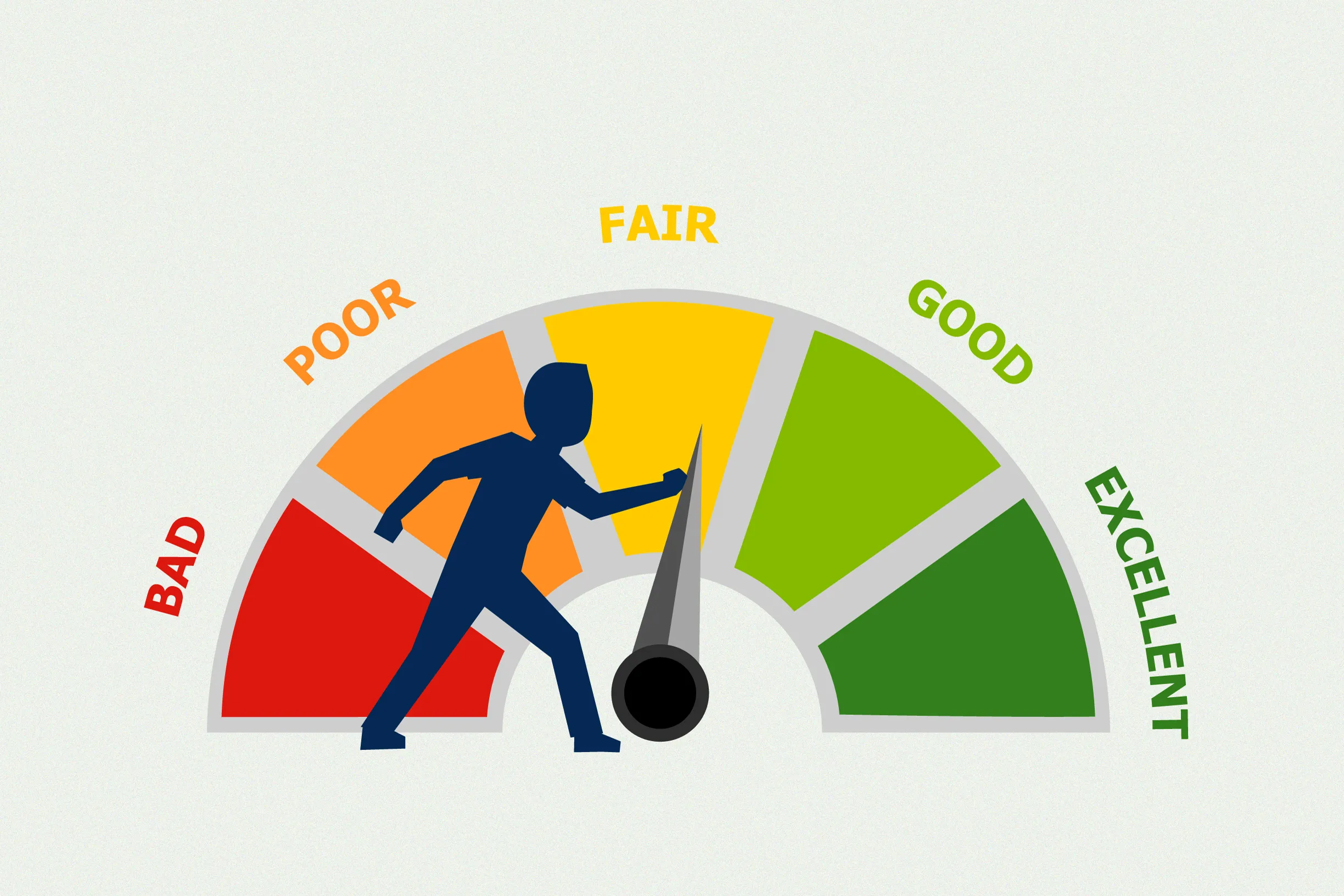

In Australia, credit scores typically range from 0 to 1,200. The higher your score, the better your credit rating, and the more likely you are to be approved for credit on favorable terms.

Credit score ranges in Australia are generally categorized as follows:

- Excellent: 833-1,200

- Very Good: 726-832

- Good: 622-725

- Average: 510-621

- Below Average: 0-509

Your credit score can be affected by several factors, including:

- Repayment History: Consistently paying your bills on time boosts your score.

- Credit Utilization: The ratio of your credit card balance to your credit limit. Keeping your credit utilization low can improve your score.

- Credit Inquiries: Numerous applications for credit within a short period can negatively impact your score.

- Credit Mix: Having a diverse mix of credit types (credit cards, personal loans, mortgages) can positively impact your score.

- Length of Credit History: A longer credit history generally results in a higher score, as it gives lenders a better picture of your credit management habits.

How Can You Check Your Credit Report in Australia?

In Australia, you’re entitled to one free credit report per year from each of the three major credit reporting agencies (Equifax, Experian, and illion).

You can also request a free report if you’ve been refused credit in the past 90 days or if you’ve had an application for credit refused.

To request your credit report, you will need to provide personal identification details such as your full name, address, and date of birth.

You may also need to provide additional documentation, such as a driver’s license or utility bills, to verify your identity.

→ SEE ALSO: Using Your Bankwest Debit Card Abroad: The Lowdown

How to Improve Your Credit Score?

Improving your credit score can take time, but it’s essential for better financial opportunities.

Here are some strategies to enhance your credit score in Australia:

- Pay Bills on Time: Timely payments are crucial for maintaining and improving your credit score. Set reminders or automate payments to avoid missing due dates.

- Reduce Outstanding Debt: Aim to pay off any outstanding debts, especially high-interest debts like credit card balances. Reducing your credit card balance will lower your credit utilization ratio, which can positively impact your score.

- Limit Credit Applications: Applying for multiple loans or credit cards within a short time can negatively affect your credit score. Only apply for credit when necessary.

- Check for Errors: Mistakes can occur in your credit report. If you spot any errors, such as incorrect personal information or wrongly reported late payments, contact the credit reporting agency to have them corrected.

- Maintain a Good Credit History: Keeping older accounts open and in good standing can help your credit score over time. A longer credit history with a solid repayment track record boosts your creditworthiness.

- Manage Credit Limits Wisely: Even if you’re not using all your available credit, having high credit limits can be viewed negatively by lenders. Consider lowering your limits if you think it might affect your credit score.

The Importance of Credit Reports for Australian Consumers

Your credit report serves as a financial passport in Australia, allowing lenders to assess your ability to manage credit responsibly.

It can affect your ability to secure loans for large purchases like homes or cars, get approved for rental agreements, or even negotiate favorable terms for credit cards and personal loans.

In some cases, employers may also check your credit report as part of their hiring process.

Having a strong credit score opens the door to more financial opportunities and better interest rates. On the other hand, a low score can limit your options and lead to higher borrowing costs.

Understanding how credit reporting works and taking proactive steps to manage your credit score is essential for long-term financial health.

Conclusion

Credit reports are a fundamental part of the financial landscape in Australia. They provide an in-depth view of your credit history and are used by lenders to assess your risk as a borrower.

By understanding what goes into your credit report and how to manage your credit score, you can improve your financial standing and access better credit opportunities in the future.

Regularly checking your credit report, addressing any discrepancies, and following good credit habits can help you maintain a healthy credit profile, ensuring you’re in a strong position when you need to apply for credit.

→ SEE ALSO: The Safety of OFX in Australia: What You Need to Know

Linda Carter is a writer and financial consultant specializing in economics, personal finance, and investment strategies. With years of experience helping individuals and businesses make complex financial decisions, Linda provides practical analyses and guidance on the Meaning of Dreaming platform. Her goal is to empower readers with the knowledge needed to achieve financial success.